Nvidia trades at 24x forward earnings, well below its 5-year average, while Kalshi traders bet its chip rental prices have peaked. Here’s the full picture.

IMPORTANT EDITORIAL NOTE: This article summarises publicly available analyst views and market data as of June 22, 2026. Nothing in this article constitutes investment advice. Readers should consult a qualified financial professional before making any investment decision.

INTRODUCTION

Nvidia is simultaneously one of the most dominant companies in the history of technology and one of the more confusing stocks to make sense of right now.

On one side: Morningstar’s senior equity analyst Brian Colello, writing on June 17, 2026, calls Nvidia “too cheap to ignore”, setting a $280 fair value estimate on a stock trading around $209, and arguing that the market is substantially underpricing a company with an 80% share of the AI accelerator market and fiscal 2027 earnings expected to grow 75% year over year.

On the other: prediction market traders on Kalshi are betting that the price of Nvidia’s flagship B200 chip commands per hour of compute has peaked for this quarter, down from $6.11 on May 30 to $4.22 by June 21, a drop of roughly 31% in three weeks. And while the broader semiconductor sector has surged as much as 84% in 2026, Nvidia itself has slipped about 3% over the past month.

This is not a simple story about an AI stock going up or down. It is a story about the tension between long-term structural dominance and short-term pricing power, and the two sides are in genuine disagreement right now.

WHAT MORNINGSTAR IS SAYING: “TOO CHEAP TO IGNORE”

Morningstar analyst Brian Colello published his “too cheap to ignore” characterisation of Nvidia on June 17, 2026, a rating that rests on three interconnected arguments.

First, valuation. Nvidia trades at approximately 24 times forward earnings, which is significantly below its five-year average of 36.6 times, according to Dow Jones Market Data cited in Barron’s. For a company with Wall Street consensus expecting 75% earnings growth in fiscal 2027 (to $8.35 per share, from $4.77 in fiscal 2026), a below-average earnings multiple represents an unusual combination. Colello’s assessment, in his own words: “We don’t foresee a slowdown in AI demand, and the company’s leadership position in the AI infrastructure market remains secure. In turn, we believe the market underappreciates its prospects.”

Second, the competitive moat. Nvidia’s CUDA software ecosystem is central to Morningstar’s thesis. As J.P. Morgan’s Meera Pandit has noted, “Every engineer and every model was trained on Nvidia’s ecosystem, including CUDA, the software layer between the chips and the code that contains thousands of prebuilt libraries for splitting workloads among chips, managing memory, and debugging.” Switching costs are high, and competing platforms, AMD’s ROCm, Intel’s oneAPI, have not yet closed the gap.

Third, the market share picture. Nvidia holds approximately 80% of the AI accelerator market today (some estimates put it at 90% in training workloads). Morningstar projects this declining to around 68% by 2030, but within a total AI spending pool that is itself expected to quadruple. The pie gets much bigger even as Nvidia’s slice gets somewhat smaller.

Morningstar’s price targets are:

- Base case: $280 per share

- Bull case: $420 per share (assumes Nvidia concedes no market share, reaching $1 trillion in annual revenue by 2030)

- Bear case: $180 per share (assumes AI demand disappoints or custom chips take significant share faster than expected)

At approximately $209 as of mid-June, the stock sits meaningfully below Morningstar’s base case. The median Wall Street analyst target price is approximately $300, implying roughly 42% upside from current levels, according to Motley Fool’s compilation of consensus data.

WHAT BARRON’S IS TRACKING: THE RELATIVE UNDERPERFORMANCE QUESTION

Barron’s recent analysis focuses on the gap between Nvidia’s performance and the broader semiconductor sector, a gap that has widened considerably in 2026.

The VanEck Semiconductor ETF (SMH) has gained approximately 84% in 2026. The iShares Semiconductor ETF has risen roughly 70%. Nvidia itself is up around 12–21% year to date, depending on the exact measurement date, a meaningful positive return, but one that has dramatically underperformed the sector it supposedly leads.

The underperformance is partly explained by the market’s current rotation. Investment dollars that might previously have flowed to Nvidia have moved toward memory chipmakers, Micron Technology and SanDisk have both risen close to 60% in the past month alone, as investors focus on the memory chip shortage and AI infrastructure buildout rather than pure GPU compute.

As James Demmert, chief investment officer at Main Street Research, wrote for Barron’s: “Even though Nvidia’s stock has performed well so far this year, there is inherent skepticism embedded in this name, principally because of the run the stock has seen over the past few years.” That skepticism, three years of extraordinary outperformance creating a mental anchor, is part of what Morningstar’s Colello argues is suppressing the stock’s valuation.

WHAT KALSHI TRADERS ARE BETTING: COMPUTE PRICES HAVE PEAKED

The Kalshi dimension of this story is the most novel and deserves careful explanation.

Kalshi is a regulated prediction market platform where traders buy and sell contracts tied to specific real-world outcomes. One of its active contracts tracks whether Nvidia’s B200 GPU compute price, measured by Ornn’s index of hourly rental rates, will close the second quarter (ending June 30) above a specific level.

As of June 22, traders on this contract have turned decisively pessimistic. The B200’s compute rate peaked at $6.11 per hour on May 30, then fell to $4.22 by June 21, a drop of approximately 31% in three weeks. Kalshi traders are now betting that the price will not recover above its May peak before the quarter closes.

What does this actually measure? Most companies access Nvidia’s GPUs not by buying the hardware outright, but by renting compute time from cloud providers and neoclouds, specialist AI infrastructure companies. The hourly rate for B200 compute is therefore a direct measure of how much the market is currently willing to pay for Nvidia’s most capable chip. When it falls, it suggests either that supply is increasing, that demand is softening, or that alternative compute options are becoming more attractive.

Ornn co-founder Kush Bavaria has described compute as becoming “a commodity class on par with energy and metals”, a framing that, if it proves accurate, has significant long-term implications for the pricing power that underlies much of the bull case for Nvidia.

Finance professor Seoyoung Kim, quoted by TipRanks, noted that “both customers and suppliers remain uncertain about future demand for AI computing”, which is reflected in the Kalshi contract’s current bearish pricing.

One important caveat: CNBC, which first reported the Kalshi contract details, discloses a commercial relationship with Kalshi that includes a minority investment. The Kalshi signal is real market data, but its amplification through CNBC’s coverage is not without commercial context.

THE GOOGLE-SPACEX DEAL: WHAT IT SIGNALS ABOUT NVIDIA’S POSITION

In the middle of this bearish Kalshi bet, a landmark deal reinforced the bull case.

Google agreed this month to pay SpaceX approximately $920 million per month to rent AI computing capacity from October 2026 through June 2029, a contract that involves roughly 110,000 Nvidia GPUs, CPUs, memory, and related components.

RBC Capital Markets used the deal to reiterate its bullish position on Nvidia. “Regardless of the precise rationale, these GPU rental agreements should put to rest lingering concerns about NVDA losing share to application-specific integrated circuits, at least in the short term,” RBC’s analysts wrote. The deal signals that even companies with their own custom chip programs, Google builds its own Tensor Processing Units, continue to rely on Nvidia at massive scale when they need to add capacity quickly.

This is the core tension of the current moment: the Kalshi traders betting on lower compute prices and the RBC analysts citing the Google deal as evidence of sustained Nvidia dominance are looking at the same company and drawing opposite near-term conclusions. Both are supported by real data.

THE FINANCIAL PICTURE HEADING INTO AUGUST EARNINGS

Nvidia’s next major reporting date is its expected earnings release on August 26, 2026. Current Wall Street consensus:

- Earnings per share: $2.06 (versus $1.04 in the same quarter last year, roughly doubling)

- Revenue: approximately $91.70 billion (versus $46.74 billion a year earlier)

- Forward price-to-earnings: approximately 24–32 times (varying by source and exact calculation date)

- Market capitalisation: approximately $5.1 trillion

In Q1 2026, Nvidia reported revenue of $81.6 billion (up 85% year over year) and non-GAAP earnings of $1.87 per diluted share (up 140%). Momentum is not the question, the question is whether the market has already priced in everything that is predictable, or whether Morningstar is correct that it has not.

Analyst consensus remains firmly in buy territory, according to multiple sources. Median target price: approximately $300. Specific ratings include China Renaissance (Buy, $319 target, initiated June 5), Needham (Buy, $270 target, reiterated June 2), and DA Davidson (Buy, $300 target, reiterated June 1).

AMD AND INTEL: THE COMPETITIVE CONTEXT

Barron’s recent coverage placed Nvidia’s valuation discussion in the context of AMD and Intel, and the comparison is instructive.

AMD has risen approximately 114% in 2026 on the strength of its growing AI chip business, with Q1 2026 revenue growth of 38% and a Q2 2026 revenue growth forecast of 46%. AMD trades at approximately 30 times forward earnings. Nvidia trades at approximately 24 times. As Motley Fool and Nasdaq have both noted, AMD is therefore more expensive on a forward earnings basis than Nvidia, despite growing more slowly. Whether AMD’s premium is justified depends on whether its trajectory, winning GPU deals with OpenAI and Meta, can close the gap with Nvidia’s ecosystem lock-in.

Intel is a separate story. Its recent recovery has been fuelled by data centre server CPU demand and the confirmation of its Intel Foundry partnership with Apple for US chip production. Its competitive position in AI accelerators remains fundamentally different from Nvidia’s.

Nvidia’s PEG ratio (price-to-earnings-to-growth) of approximately 0.68 is below AMD’s 1.09, according to Yahoo Finance data cited by Motley Fool. A PEG ratio below 1 conventionally suggests a stock is undervalued relative to its growth trajectory.

WHAT THE MARKET SEEMS TO BE PRICING IN

Putting this together, the current market appears to be pricing Nvidia at a significant discount to both its historical valuation and its projected earnings growth, for a combination of reasons:

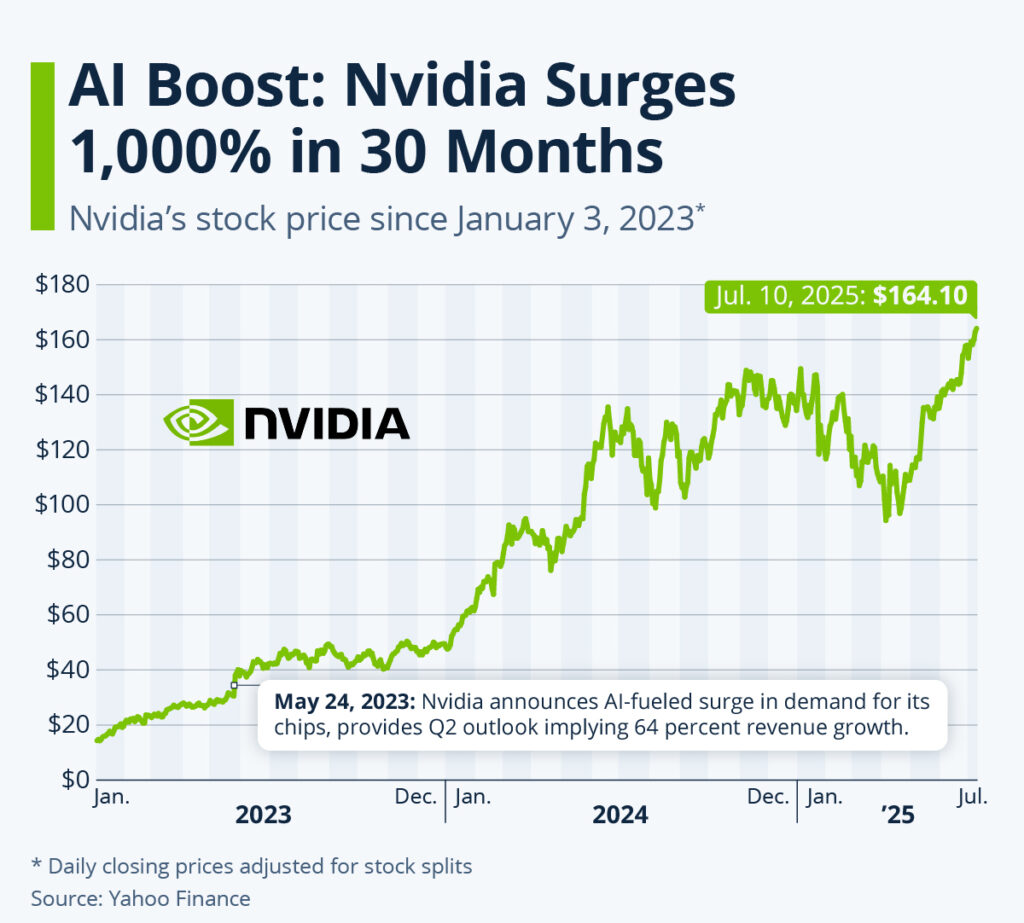

- Psychological skepticism about a stock that has already risen over 1,200% since 2023, creating an anchoring effect

- The rotation toward memory chips (Micron, SanDisk), which are the current focal point of the AI infrastructure buildout

- The Kalshi signal that B200 compute prices may be softening, suggesting potential pricing power limits

- Longer-term uncertainty about whether Google’s TPUs, Amazon’s Trainium, and other custom silicon will eventually capture meaningful training share

None of these concerns are irrational. All of them are also contested by the bull case.

CONCLUSION

Nvidia is not a simple story, and this article does not attempt to make it one.

What the data shows clearly: a company expected to grow earnings 75% in fiscal 2027 trading at 24 times forward earnings, below its five-year average, while the sector it leads has more than tripled that return year to date. Morningstar’s Colello calls that gap a buying opportunity. Kalshi traders are betting the near-term compute pricing story is less favourable than bulls expect.

What happens next depends substantially on the August 26 earnings report, which will either confirm the revenue trajectory Wall Street is expecting or introduce the kind of guidance uncertainty that has historically closed valuation gaps quickly.

None of this is investment advice. It is a picture of what analysts, market data, and prediction markets are collectively saying about one of the most important companies in the current technology cycle. The full breakdown of those perspectives, with all sources clearly cited, is in the article above.

If you found this analysis useful, see also our coverage of the AI memory chip shortage driving iPhone price increases, and the broader semiconductor market dynamics affecting consumer electronics pricing across 2026.

{kind=link}